As in my prior commentary, AI is coming to be an everyday term not only from the science fiction of movies, but increasingly from the realities of our everyday lives.

Many debates are in play around AI, where it can be trusted, how robust it is and the impact if may have on all our lives and job roles in the coming years. It is inherently linked to the concept of robotics and ability for a human like machine to mimic our human form and actions.

AI by many is expected to bring fear and negative impact, to replace the human in many job of today and to make others lazy where affordability allows them to have machines do mundane and boring tasks for them. As the human form strives forwards for an easier more productive life AI will invariably continue to invade, be it under the cover guise of other non-AI labelled devices.

41% of consumers believe artificial intelligence will improve their lives in some way. (Source: strategy Analytics)

As this advances the question of where we shall and shall not trust machines and AI will continue to develop with trust gains invariably coming over time through familiarity and complacency. It was not so many years ago that there was general fear of the introduction of cashpoints, with most preferring the human teller. This continued when internet banking was untrusted by the masses where in 2007 only 30% were using it, until today where 2020 saw 76% of UK adults using internet banking.

Are we going to put increasing trust in AI? Does it have accountability to be trusted? In the finance arena human run institutions have been held accountable for centuries. We have trusted humans to learn and take action with autonomy of our finances, but in these instances, we can determine blame with accountability here required. Humans have held responsibility, but not been infallible to error. So shall we trust AI to be responsible? We already do so to some great degree, every time we invoke a Siri or Alexa search we trust the results given as we are not eyeballing the search engine results and scanning from a broad range of answers. We are allowing these AI assistants to autonomously provide us the best result deemed by them not us!

AI in driverless vehicles is progressing despite human fatalities. In these instances, the incident, reasons and data are very public, being that we are dealing with risk to human life itself. This industry is heavily regulated unlike the software generic software industry where we are all too familiar with the very public debate on social media networks and the manipulation, they van bring to important global matters such as the USA election. As we see AI penetrating across industry sectors, we can expect to see a drive for greater regulation and accountability for damage caused. We have to avoid the ability for software producers to shirk responsibility and liability of AI’s outcomes through claim of the autonomy it acted under.

AI is an attractive proposition for the benefits it can bring in cost reduction (often through automating actions that remove the need for a repeatedly paid human) and its ability to perform tasks repetitively with huge data assimilations without effect of boredom or fatigue.

AI implementation in consumer-packaged goods has led to a 20% reduction in forecast errors. (Source: Forbes)

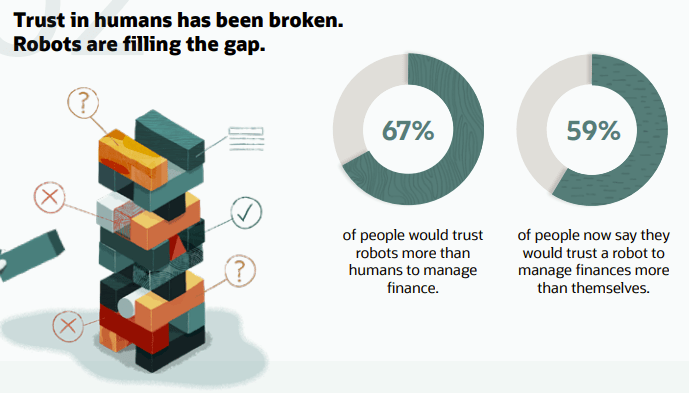

This lends itself to the findings of a new study by Oracle and personal finance expert Farnoosh Torabi where trends indicate that finance is going to be a major benefactor of AI as will its customers.

We are at the dawn of a new AI driven financial world where indication is that we will trust finance AI more than a human counterpart. Whilst this may through doubt and sceptism of consumer acceptance, as already illustrated we have been here before in the financial community with the likes of the cashpoint machine and internet banking. The trend is to refute, doubt and question and find that resistance is quickly overcome by use and benefit realisation.

For example, trust of human actors in finance is waning, after all it is the human that invokes the negative sides of finance; fraud, identify theft and emotive error in judgement. When you accept that actually much of the protection against the ‘human finance threat’ comes from AI it flips the table of receptiveness.

75% of companies plan to use AI systems to eliminate fraud. (Source: Aiiot)

Financial processes and interactions have increasingly been digitally led over recent years and we have witnessed a trend for a less human to human financial interaction. Consider the % of online purchase transactions via the likes of Amazon, Ebay and Paypal. We even witness the buying of high-cost items such as cars online and unseen, something unheard of not so long ago. For banking less and less interactions are in person at a physical bank location being replaced by a cashless trusting approach, again something in recent years a rarity, now commonplace. This has distanced our interaction with real physical money even further and driven greater acceptance to new financial processes.

Human’s are change resistant, until the change benefit outweighs the perceived pain and risk. This is not a new cycle and will not be continue to repeat as innovation drives forwards.

Adoption of new processes and technology has been accelerated by the impact of COVID where we have been pushed to an increasingly distanced interaction and found that we are capable of doing far more electronically, than perhaps many thought or were willing to trust.

Banking will be one of the two industries that will spend the most on AI solutions by 2024 (IDC)

When it comes to money people are already indicating trust for AI and robotic advice over their own and that of human financial advisors. This will re-shape the role of those in finance and traditional institutions, driving success for those embracing the new and increasing risk for those who focus on traditional finance processes and serving the diminishing customers seeking such.

The full report can be accessed here.